Digital assets have firmly entered financial circulation: they are used for capital preservation, payment for services abroad, and investments. But sooner or later any crypto holder faces a practical task: how to turn virtual coins into real rubles on their bank card.

In Russia, the circulation of cryptocurrency is not outside the law, however it falls under financial regulation norms. When converting USDT or Bitcoin into fiat rubles and subsequently crediting them to a bank account, it is necessary to take into account financial monitoring rules and the requirements of credit organizations for client identification. That is why today users are looking not simply for fast, but for fully transparent and legal exchange methods.

There are several proven conversion schemes: from decentralized P2P platforms to specialized exchange services. Regardless of the method, the path of funds always looks the same: the crypto leaves the personal wallet, passes through an exchange, and arrives on the card already in the form of rubles.

To carry out this procedure without the risk of blocks and unnecessary questions from the bank, it is important to understand three key aspects:

- Which exchange options make it possible to receive exactly cash on the card?

- How is the process of transferring money through a bank technically arranged?

- What legislative norms must be followed in order not to violate the law?

What the law says about cryptocurrency in Russia

")

Status of digital money

From the point of view of Russian law, cryptocurrency is a digital currency that is recognized as property. It exists exclusively in the form of records in the blockchain network and is not a legal means of payment (you cannot pay with bitcoins in a store). However, owning it, storing it in wallets, and conducting transactions is permitted.

Stablecoins (for example, USDT) are the most popular when withdrawing funds. Their rate is pegged to the dollar, which makes them an ideal bridge for subsequent conversion into rubles without the risk of losing money due to volatility.

Permitted actions with assets

Russian legislation allows citizens to conduct the following operations with crypto:

- Acquire and dispose of (sell) digital assets.

- Transfer them between wallets.

- Exchange them for other assets or fiat through third-party services.

- Use them as an investment asset.

Thus, the sale of cryptocurrency for rubles itself is legal. This is regarded as the sale of property, which entails only tax consequences (the obligation to declare income), but not administrative or criminal liability.

Why a bank may block a transfer

It is important to understand: a direct “crypto → card” transfer does not exist. The banking system operates only with fiat money. Therefore, you first sell the asset (for example through an exchange service), and only after that receive an ordinary money transfer from the buyer or service to your card.

From the bank’s point of view, this is simply a receipt of rubles to the account. However, if the amount is large or the transfer has signs of suspicious activity, the financial organization has the right to request confirmation of the origin of the funds. This is not a ban on crypto, but a standard procedure under Federal Law 115-FZ (counteracting money laundering).

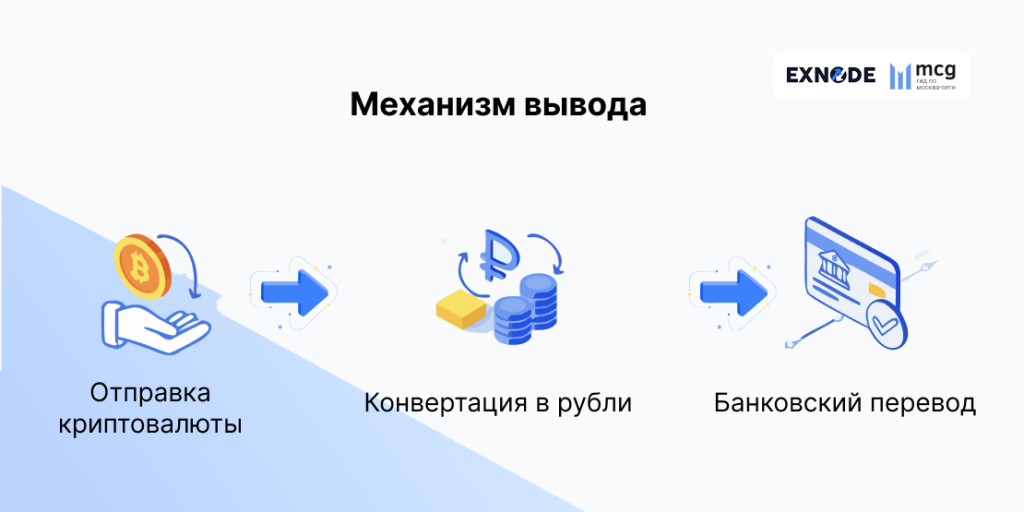

How withdrawal mechanisms work: from wallet to card

The essence of the cash-out process

The phrase “withdraw crypto to a card” technically means double conversion. First you exchange the digital asset (for example ether or USDT) for rubles, and then send these rubles to the recipient via a bank transfer.

The process always requires the participation of an intermediary: an exchange, P2P platform, or exchanger. You send crypto from your wallet to the service account, after which the service (or another user) transfers the equivalent amount in rubles to you by non-cash settlement.

What the final rate depends on

The final amount that will arrive on the card consists not only of the exchange rate. Three factors influence it:

- Market price. The value of the asset on leading exchanges (Binance, Bybit, etc.) is taken as the basis.

- Platform liquidity. On large platforms with a high trading volume the difference between the purchase and sale price (spread) is minimal, which is beneficial for you.

- Intermediary commission. Each service takes its own margin. In some cases it is included in the rate, in others it is indicated separately as a percentage of the transaction.

Step-by-step scheme for withdrawing money

Any legal withdrawal of funds to a card fits into three sequential stages:

- Asset transfer. You initiate a transaction from your cold or hot wallet to the address specified by the exchange service or exchange. Usually USDT (in the TRC20 network) is used for this because of the low commission and speed.

- Exchange for rubles. The platform conducts the deal: either through a counter order with another user (P2P), or at the expense of its own reserves (exchanger).

- Credit to the card. After the exchange is completed the service sends rubles to your card (most often via the Faster Payments System or a transfer by card number). At this stage the cryptocurrency part of the path ends, and you receive ordinary fiat money.

Main ways to convert digital currency into rubles

Three main legal ways of exchanging into fiat rubles with crediting to a card have developed on the Russian market. The choice of a specific tool depends on the amount, urgency, and the technical preparation of the user.

Ways to withdraw cryptocurrency

| Method | Commission | Speed | Suitable for |

|---|---|---|---|

| Exchangers | 1–3% | 5–20 min | beginners |

| Exchanges | 0.1–1% | 10–60 min | traders |

| P2P | minimal | 10–40 min | experienced users |

Let us examine each method from the simplest to the more complex.

Online cryptocurrency exchangers: a balance of speed and simplicity

For most users the simplest tool remains specialized exchange services. These are intermediary services that take on all the technical work of conversion.

How crypto exchangers work

- The user goes to the exchanger website.

- Selects the direction (for example USDT → RUB), indicates the amount and card details for crediting. The service instantly shows the rate and the exact amount to be paid.

- After creating the request the user sends cryptocurrency from the personal wallet to the service address.

- The operator checks the receipt of funds in the blockchain network and initiates a bank transfer to the client’s card.

The entire chain usually takes from 5 to 20 minutes.

What parameters influence exchange conditions

When choosing a service it is worth paying attention to four key characteristics:

- Rate. It may differ from the exchange rate by 1–3% — this is the service’s earnings.

- Commission. Some exchangers take an explicit commission above the rate, others include it in the difference between purchase and sale rates.

- Operation limits. Each service has a minimum and maximum transaction amount. For large amounts (from 500 thousand rubles) the conditions are often discussed individually.

- Transaction speed. Depends on the load of the blockchain network and the responsiveness of the support service.

Why users use monitoring services

Since hundreds of exchange services operate in Russia, users actively use aggregators (monitorings). These sites collect in real time the rates and availability of reserves from different crypto exchangers, allowing the selection of the best conditions. Among the services that are often found in aggregators users mention “BukhtaObmena”, “ChangeExpert”, and “Finex24”. Monitorings also show reviews and the operating time of the service, which reduces the risks of encountering fraudsters.

Cryptocurrency exchanges: maximum reliability and liquidity

Exchanges are a professional tool for working with digital assets. They are suitable for those who trade regularly and are ready to undergo full verification.

How withdrawal through an exchange works

The user registers on a trading platform (for example Bybit), transfers cryptocurrency from the personal wallet to the exchange account, and places a sell order in a pair with the ruble. After a buyer is found the rubles are credited to the exchange fiat balance. Then the user withdraws these funds to their bank card.

User verification requirements (KYC)

")

To work with rubles exchanges are obliged to identify the client’s identity. Without passing KYC (providing passport data and a selfie), withdrawing fiat funds to a Russian bank card will most likely not be possible. This is a requirement of financial regulation and of the partner banks themselves.

Advantages and limitations of exchange withdrawals

| Advantages | Limitations |

|---|---|

| The best market rate. High liquidity guarantees a minimal spread. | Full transparency. The bank sees that the transfer came from an exchange. For the tax service this is a plus, for those who want to remain unnoticed it is a minus. |

| Reliability. Large exchanges bear reputational risks and do not disappear with clients’ money. | Commissions. The exchange charges a fixed fee for the ruble withdrawal transaction. |

| Automation. Deals are executed instantly without the participation of an operator. | Sanctions risks. Some platforms have introduced restrictions for Russian users. |

P2P platforms for cryptocurrency exchange: flexibility and control

P2P (peer-to-peer) is a model of direct deals between people. The platform here acts only as a guarantor of security.

What P2P exchange is

This is a trading platform (built into an exchange or a separate service) where sellers and buyers themselves set the conditions. You can sell USDT at a price higher than the exchange rate if you find a buyer willing to pay that price for a convenient transfer method.

How a P2P transaction takes place

The mechanism of any P2P transaction is standardized and consists of four steps:

- The user selects an offer. The buyer searches for an advertisement with a suitable rate and payment method (for example transfer to Sber or the Faster Payments System).

- Cryptocurrency is locked in escrow. As soon as the buyer presses “Buy”, the platform locks the seller’s cryptocurrency in its account. No one can use it until the transaction is completed.

- The buyer transfers rubles. The buyer sends the agreed amount to the seller’s card by a regular bank transfer.

- The completion of the transaction is confirmed. The seller checks the receipt of money and presses the confirmation button. The platform unlocks the cryptocurrency and transfers it to the buyer.

When P2P is used most often

This method is popular among those who value confidentiality (do not want to show their passport on an exchange) and are ready to spend time searching for a favorable rate. P2P is also indispensable when it is necessary to receive rubles on a card of a bank with which large exchanges do not have direct cooperation. However, here the risk of encountering fraudsters is higher, therefore it is important to carefully check the rating of the counterparty.

Which bank cards are suitable for withdrawing cryptocurrency

Even if you have successfully exchanged USDT for rubles, the final stage — crediting the money to the card — may raise questions from the bank. Credit organizations view operations related to digital assets differently. Understanding their internal policy will help avoid blocks and claims.

Which banks support cryptocurrency-related operations: actual practice

Formally no Russian bank has announced a ban on crediting rubles obtained from the sale of cryptocurrency. However, in practice attitudes toward such transactions differ. Banks look not at the origin of the crypto (they do not see it), but at the behavior patterns of the recipient.

Taking into account current market practice and user experience, cards of large Russian banks are most often used to credit funds after the conversion of crypto assets.

T-Bank

T-Bank (formerly Tinkoff). In user communities it is often called one of the most convenient banks for operations related to P2P transfers and exchange services. The developed infrastructure of the faster payments system allows transfers to be received quickly. At the same time mass receipts from a large number of senders may cause additional checks.

SberBank

Sber traditionally adheres to a more conservative approach to operations that may be associated with high turnover between individuals. Large amounts or frequent transfers from unfamiliar senders sometimes become a reason to clarify the origin of funds.

Alfa-Bank

Users note that transfers to Alfa-Bank from large services or trading platforms usually pass without difficulty, however with active P2P operations the bank may request additional information about the nature of the operations.

Raiffeisenbank

Raiffeisenbank and UniCredit Bank. Previously they were actively used for such operations, however because of sanctions restrictions and changes in international transfers their popularity among crypto investors has decreased in recent years.

VTB, PSB and Otkritie

Large state banks as a rule operate under stricter internal financial monitoring regulations. When transferring significant amounts or atypical turnover on the account the client may be asked to confirm the source of funds.

Why banks may check cryptocurrency withdrawal operations

Any bank is obliged to comply with Federal Law No. 115-FZ “On counteracting the legalization (laundering) of proceeds”. This is the main reason why operations fall under control. Security service employees look not at where the cryptocurrency transfer came from (they technically cannot track this), but at atypical account behavior.

What may cause suspicion:

- A sharp increase in turnover. If usually 20–30 thousand per month passed through the card and suddenly 300 thousand from an unfamiliar sender arrives — this is a trigger for verification.

- Many transfers from different individuals. A characteristic sign of P2P trading or receiving funds from clients. If 20 different people transferred money to you in one day the algorithm may regard it as entrepreneurial activity without registration.

- Transfers in uneven amounts. Receiving sums such as 9,876.54 rubles (after conversion with commission) looks more suspicious than even 10,000 or 15,000 rubles.

In which cases card blocking is possible

Blocking (or restriction of remote service) occurs when the bank cannot clearly classify the operation. The most frequent scenarios:

- Suspicion of fraud. If the sender of the money claims that they became a victim of deception (relevant for P2P if you encounter a “fake” buyer), the seller’s bank may temporarily block the account until clarification.

- Violation of limits. Many banks have unofficial limits on incoming transfers from individuals. Exceeding them without explanation leads to card blocking and a request for documents.

- Failure to provide supporting documents. If the bank requested confirmation of the origin of funds and the client could not explain where the money came from (did not show screenshots of transactions on the exchange or an agreement with an exchanger), the card may be blocked.

How to reduce risks:

- Use a separate card for crypto assets without mixing it with salary and credit accounts.

- Try to withdraw funds not too often and in approximately equal amounts if possible.

- Save screenshots of deals and correspondence — they will help when dealing with the bank.

Risks and ways to minimize them when withdrawing digital currency to a card

Operations at the intersection of digital assets and the banking system are traditionally associated with additional risks — from user mistakes to blocks by financial organizations. In practice losses are more often associated not with market volatility but with user errors or working with unscrupulous services.

Main signs of unreliable services

Choosing an unverified crypto exchanger or P2P intermediary is the main reason for losing money. Fraudsters or simply unscrupulous services can be recognized by a number of characteristic signs.

- Too favorable rate. If the rate in an exchange service is 5–10% better than the market average this is almost always a trap. Fraudsters lure victims with abnormally high quotations after which they either disappear with the money or begin to demand “additional commissions” to complete the transaction.

- Absence or falsity of licenses and documents. Legal services usually operate transparently: they indicate legal information and have a public offer and privacy policy. If there is nothing on the site except a form for entering the amount this is a reason to be cautious.

- No support or strange communication. Try writing to support before the deal. If they respond with templates or slowly it is better to look for another service.

- Short lifetime of the site. The age of the domain can be checked through specialized services. If the service is only a month old but offers huge limits it is not worth risking.

User mistakes in cryptocurrency transfers

Even when working with a reliable service you can lose money or fall under a block if simple rules are violated. Here are the most common mistakes.

- Sending to the wrong network. Cryptocurrencies exist in different blockchains: USDT exists in TRC20, ERC20, BEP20 networks and others. Sending coins through the wrong protocol (for example to a TRC20 address while selecting the ERC20 network) risks losing funds. To recover them you will have to contact support and it is not guaranteed they will be able to help. Always double-check the network before sending.

- Ignoring bank limits. Banks may block operations that look suspicious. If you split a large amount into dozens of small transfers hoping to remain unnoticed this actually attracts the attention of the security service. It is better to conduct one large transparent deal through a reliable exchanger than 20 small ones.

- Lack of supporting documents. Screenshots of correspondence, exchange orders, payment receipts — all of this must be saved. In case of card blocking and a request from the bank these documents will become the only proof of the legality of the funds.

- Haste in transactions. The main mistake is confirming receipt of fiat before the money actually arrives in the account and becomes available. Fraudsters may send a fake notification of transfer. Always check the card balance in the bank application and do not rely on SMS or screenshots.

Frequently asked questions about withdrawing cryptocurrency into rubles

Is it necessary to pay tax when selling cryptocurrency?

Yes. If you sold digital assets at a higher price than you bought them the resulting difference is considered income. In Russia cryptocurrency is equated with property therefore profit is subject to personal income tax. If transactions did not bring profit or were unprofitable the tax obligation does not arise, but with large turnovers it is recommended to keep documents of purchase and sale.

Is it possible to receive money for cryptocurrency on another person’s card?

Technically the transfer is possible however it increases the risk of account blocking. The bank may require the card owner rather than the actual seller of the crypto asset to explain the origin of the funds. In disputed situations it will be difficult to prove that the money belongs to you. It is safer to use a card issued in your own name.

Are there restrictions on the withdrawal amount?

There is no nationwide limit. Restrictions are set by individual participants in the process: exchangers set transaction limits, exchanges set daily withdrawal limits, banks set internal financial monitoring thresholds. For large amounts transactions may take longer and may be accompanied by additional checks.

How long should orders and receipts be stored when withdrawing and why are they needed?

Screenshots of orders, receipts, and correspondence should preferably be stored for at least several years. They may be required by the bank when verifying the origin of funds or by tax authorities when declaring income. Without such confirmations it is significantly more difficult to prove the legality of operations.

Is it possible to withdraw cryptocurrency directly to a bank account without intermediaries?

No. The banking system works only with fiat currencies therefore digital assets are always first sold through an exchange, exchanger, or P2P platform. The account receives ordinary rubles from another individual or service. A direct channel “blockchain → bank card” does not exist.

Conclusion

Withdrawing cryptocurrency into rubles to a bank card in Russia is a technically simple and quite legal process if approached with an understanding of the basic rules. Legislation considers digital assets as property therefore their sale for fiat is not prohibited. The main thing is to comply with financial monitoring requirements and choose reliable tools for conversion.

Today one of the most common tools remains online exchangers which can be found through aggregators offering a clear interface and fast withdrawal of funds without the need to understand the intricacies of exchange trading.

Whatever method you choose the key to success is attentiveness. Always double-check the cryptocurrency sending network, keep confirmations of transactions, and do not try to deceive the bank by splitting large amounts into small transfers. This will only attract the attention of the security service.

As the crypto market and the number of exchange services grow users increasingly have to navigate a large number of offers. In such conditions the key factor becomes not only the rate but also the transparency of operations, compliance with banking requirements, and the choice of a reliable platform.